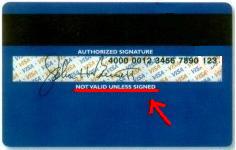

Everyone has a signature bar on the back of their credit card. You're supposed to sign it as soon as you receive the card, to authorize it for use as payment.

Many retailers have begun using this signature as a way of checking that you are the owner of the card. They compare the signature on the card to the the receipt you just signed (or pretend to) in order to verify that you are both the card signer and the receipt signer.

In this age of identity theft, some consumers don't feel that is enough. They feel picture ID is necessary, not just a signature comparison. So instead of signing their card, they write "CHECK ID" on the signature bar. The idea is that your driver's license has both your signature and your picture on it, which is even better.

But a lot of retailers don't accept this. Every day someone wants to tell me another story about the "stupid" checkout clerk at Wherever's Department Store that wouldn't accept their card because it wasn't signed. They beam from their high horse about their superior intelligence, and how the world is going to hell because stupid clerks aren't reasonable enough to understand the increased security of a picture ID and to look there for the signature.

Well, here's the deal: If your card isn't signed, it isn't authorized to be used as payment. That's why it says "authorized signature." An unsigned card is an unauthorized card. The primary intent of signing a card is not to put a biometric identifier on it (though it is that as well), the intent of signing a card is to legally state that, "yes, I authorize and accept responsibility for this card, along with a simlarly signed reciept, to pay for things against my good name." So if I were a stupid retail clerk, I wouldn't accept your unsigned card, either. Get over yourself.

Sorry for the whiny rant.

No comments:

Post a Comment